The $700 billion bailout plan has so far failed to get credit flowing freely again. And tonight, new evidence there's a complete lack of oversight of this massive Wall Street bailout. One estimate now, saying the bailout will eventually cost as much as $5 trillion, almost twice the entire federal budget. The incompetence and stupidity expodes the brain.

It just looks like for decades the United States government has been lurching from one blunder to another until we finally are engaged an irreversible downward spiral. It is imperative that we, the people, get a lot smarter, and very fast, about how to run our government, or we will forfeit our great nation and exemplary democracy (as well the our home, the earth).

How far have we fallen: American Democracy was the innovative invention of the 18th century, that people could be ruled by their own wishes and make their own destiny. It became the great advancement of the 20th century, at which beginning democratic nations in the world were only10%. Our great and bold founders gave so much careful thought, intellectual capital and brave sacrifice to form a completely original model for human self-governance. It makes my heart thump to think about them and what they created, what they thought about, cared about, wrote about and fought for, the loftiness of their purpose, the heritage they bequeathed; but then the heart aches with how we have perverted our noble inheritance into a venal pursuit of money, the lobbying for self-interests, the lowest common denominator in place of the greater good---- all that would be unrecognizable to those principled men. That is the tragedy, that in all important respects, we have squandered our noble inheritance. We have not only run our economy and global financial system into into the ditch, but we have also run our aspiring democracy and civilization into the ditch too, and with greed, hubris, and reckless disregard, turned a pristine planet of fabulous primordial habitats and species into a fetid, moribund wasteland. I feel really ashamed for my part in this degradation and the horrible loss inflicted on the innocent species for whom we are charged as guardian-protectors.

Please think about this as you read the following Partial Transcript from Lou Dobbs Tonight November 13th, 2008 (bold added for emphasis):

DOBBS: Indeed, that $5 trillion bailout may in fact be reinventing these free markets.

President Bush struggling to deal with this crisis and the number of home owners in danger of losing their homes is soaring. The number of foreclosures skyrocketed by 25 percent in the year to October. Nearly a million families have lost their homes to foreclosure since the housing crisis began in August of last year.

The highest foreclosure rates are in Arizona, Florida and Nevada. Top senators today demanding the nation's banks do much more to help home owners facing foreclosure. Those senators are criticizing as well the Treasury Department and the Federal Reserve for not disclosing critical information about the massive bailout of Wall Street.

By some estimates, the bailout could eventually cost taxpayers a staggering $5 trillion..

(BEGIN VIDEOTAPE) LISA SYLVESTER, CNN CORRESPONDENT (voice-over): The banks haven't been doing their job, according to members of the Senate Banking Committee. Instead of loaning money given under the bailout program, the senators say some financial institutions are hording the cash. And as more homes head to foreclosure, patience on Capitol Hill is running thin.

SEN. CHRISTOPHER DODD (D), CONNECTICUT: We wanted to see more progress from your friends in the financial sector. More progress in foreclosure mitigation, in affordable lending and in curbing excessive compensation. And if that progress is not forthcoming, then we are prepared to legislate.

SYLVESTER: Others criticize the lack of transparency. Banks have received the money with few strings attached. An inspector- general who is supposed to oversee the bailout program has not been appointed. And the Federal Reserve has denied a Freedom of Information Act request from Bloomberg News to disclose which firms have received $2 trillion in emergency loans, money that goes beyond the bounds of the federal bailout. And the Fed will not say what collateral banks had to put up.

STEPHEN MOORE, WALL STREET JOURNAL: We don't know where the money went. We don't what the criteria is for spending it and we don't think that there's a transparency that the public should demand when this money -- this kind of money is being spent.

SYLVESTER: Banks are reluctant to share with the public the fact that they need government help. They fear a stigma. If customers worry the institution is in trouble, it could lead to a run on the bank. The Financial Services Roundtable, an industry trade group, saying quote, "we offer transparency, but we believe to protect against contagion and possible negative reaction from consumers and investors, that sensitive information should be protected." One congressman says the public has the right to know.

REP. JEB HENSARLING (R), TEXAS: But we are talking about hundreds of billions and frankly, if you look at it closely, trillions of dollars that are being used and really used in a secret fashion.

SYLVESTER: Lots of taxpayer money on the hook. Few answers.

(END VIDEOTAPE)

SYLVESTER: The Federal Reserve would not comment on the complaints of transparency, citing an ongoing lawsuit that has been filed to compel the agency to release more information. We also contacted the Treasury Department, but officials did not return phone calls or e-mail -- Lou?

DOBBS: So there is no transparency or even a suggestion on the part of either the Federal Reserve or the Treasury Department that they want to be interfered with by the public's right to know?

SYLVESTER: Well indeed. You know, Lou, this is -- we're talking about and you can't emphasize this enough. We are talking about trillions of dollars here. And that, you know, a lot of lawmakers saying we don't know which banks are getting this money.

We don't know what they're putting up as collateral. And so they're saying -- how can we continue to justify giving this money if we don't even know if it's going to go for any good here?

DOBBS: Well there's another issue, too, and that is that without disclosure of what is happening with taxpayer money, this no longer is a democracy and we are no longer free people. And that may be the -- the direction, the determination of the Federal Reserve and this Treasury Department.

But it's about time that somebody, some elected official somewhere in Washington, D.C. decides that it's time to reassert at least the basic tenet of democracy in this society of ours.

Executives from the four banks at today's Senate hearing today insisted that none of the bailout money that they're receiving goes towards staff bonuses. The executives from Wells Fargo, Bank of America, Goldman Sachs and JPMorgan Chase promise that the bailout money will be used for loans for what they call credit-worthy borrowers.

There was no explanation about how they could tell the difference between taxpayer money and the rest of the money. Goldman Sachs CEO Lloyd Blankfein did not attend today's Senate hearing. He sent one of his underlings instead.You may remember that back in February, "The New York Post" Liz Smith reported that Blankfein had said at a dinner that this economy is doing just fine, despite all the evidence to the contrary and arguing with me on the issue.

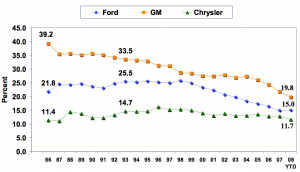

Well another highly-compensated CEO, Bob Nardeli (ph), also a self-styled genius at Chrysler, tonight is appealing for an urgent government bailout of his company. This is the same Bob Nardelli who received a severance package worth more than $200 million when he was fired from his previous job, as CEO of Home Depot. He didn't do too well there, either.

Nardelli was appointed to his job at Chrysler by the company's owners, the rather private, some would suggest overly private investment firm, Cerberus. Shares of Chrysler vehicles have plummeted over 35 percent over the past year. But they're a private company, so you can understand why a lot of people are eager to put public funding into their company.

One reason for the worsening condition of our automotive industry is the commitment of successive administrations to something that I guess we could call faith-based economic policies. So-called free trade has devastated our manufacturing industry in this country and caused millions of middle class Americans their jobs and their quality of life. Ines Ferre reports now on the latest trade deficit.

(BEGIN VIDEOTAPE)

INES FERRE, CNN CORRESPONDENT (voice-over): The total U.S. trade deficit in September went down by almost 4.5 percent, compared to August. But our deficit with China soared. More and more Americans are out of work, almost 10 million now. And fewer goods are made in the USA.

LLOYD WOOD, AMER. MANUF. TRADE ACTION COALITION: Literally, millions of opportunities for middle-class jobs have gone offshore. And until you actually start producing more in the United States, you're not going to create the middle-class jobs.

FERRE: Democrats in Congress are now pushing for a bailout for the near-bankrupt big three auto makers to prevent millions more jobs being lost. But so far, there's little indication the plan in Congress will stop the auto makers outsourcing more of their work, especially parts.

ALAN TONELSON, U.S. BUSINESS & INDUSTRY COUNCIL: (INAUDIBLE) U.S. content are not insisted upon, if they're not mandatory, Detroit and also big American parts makers will continue to go offshore and the benefits to the U.S. economy from any bailout package will be much less than is widely expected.

FERRE: The U.S. Business and Industry Council says in 2006, U.S. manufacturers imported about a third of their steering and suspension parts. The same for engines and engine parts. And almost 46 percent of lighting systems were brought in from abroad.

(END VIDEOTAPE) FERRE: And the trade balance in manufacturing is so bad that just to give you an example, between January and September of this year the U.S. imported almost five times the amount of cars that it exported.

DOBBS: It is -- it's a very unhappy equation. We use the expression balance. It's outright a deficit. Even though the economists like to talk about a balance. We haven't been near a balance in so long in this country. What is the reaction?

I mean what is -- anybody saying about the suggestion that so long as we're off-shoring so much of the production, and in this country, for Chrysler, for General Motors, for Ford and outsourcing so much of the parts work, what is the direction? Anybody talking about changing the rules here?

FERRE: Well and that's the thing. If these companies get a bailout, then would there be any kind of strings attached saying you need to create this amount of jobs, you need to have this amount of parts, American-made parts. And not just with that industry, but also all the manufacturing industries.

DOBBS: Yes, it's amazing to me how many of the so-called geniuses who have been saying that outsourcing is not a big problem. Off-shoring is not a big problem. Now that we desperately need a manufacturing base that has been reduced -- and this is important for everybody to know.

The manufacturing employment levels in this country are now at the same level as 1942. This country, we talked about the energy, energy independence. We have an absolute dependency on foreign producers in so many areas of our economy, it's staggering.

Tonight there are new doubts that the car makers will be receiving a federal bailout, at least soon. Senate Banking Committee Chairman, Senator Chris Dodd, said he doesn't believe there are enough votes in the Senate to pass a bailout for Detroit. The senator said he doesn't know a single Republican who supports the bailout.

Read More...

Summary only...